Your Knee Replacement Just Got a Software Update: The Rise of the Connected Implant

April 23, 2026

Here is a question every medtech executive should be asking right now: What happens when your product keeps talking after surgery is over?

A decade ago, a knee replacement was a piece of titanium and polyethylene. It did one job: replace a worn-out joint. The surgeon put it in, the patient rehabbed, and the device went silent until something went wrong.

That era is ending.

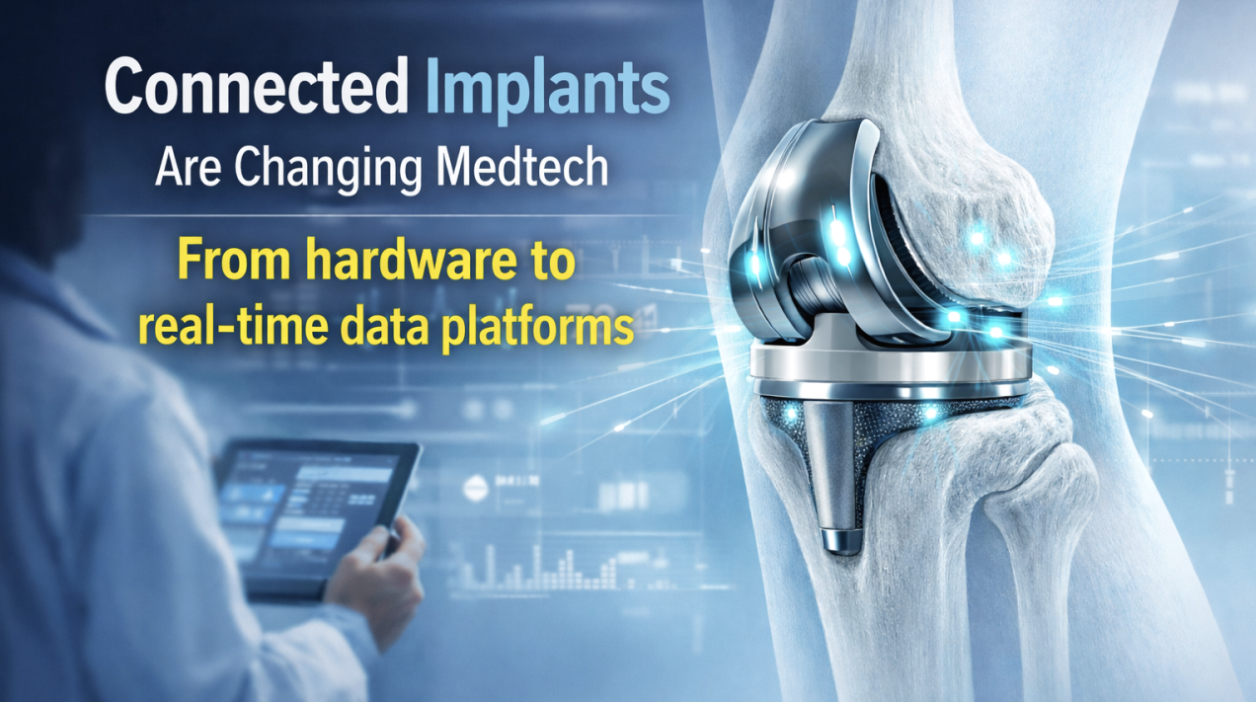

Today, smart orthopedic implants contain IoT-enabled sensors that monitor load distribution in real time, transmit data to a surgeon’s dashboard, and trigger alerts before a patient feels a thing. And it is not just knees. Connected devices are transforming cardiology, neurology, respiratory care, and drug delivery.

The numbers tell the story. The global smart orthopedic implants market was valued at $27.3 billion in 2024 and is projected to reach $38.3 billion by 2030, growing at a CAGR of 5.9% (BCC Research, MDS111A). North America alone accounts for 41.2% of that market.

This is not a niche trend. It is a fundamental shift in what it means to be a medical device company.

Three Forces Driving the Shift

The connected implant did not appear overnight. Three converging forces made it possible.

1. Sensor miniaturization

IoT-enabled sensors now fit inside hip stems, spinal fusion cages, and pacemakers without adding meaningful size or weight. They capture pressure, temperature, motion, and biochemical markers, turning passive hardware into continuous monitoring platforms.

2. AI-powered analytics

Raw sensor data is only useful if you can make sense of it. Machine learning algorithms now detect patterns that clinicians would miss: a subtle shift in gait symmetry, an unusual cardiac rhythm, early signs of implant loosening. AI-enabled monitoring is a primary market driver in the smart orthopedic space and a key emerging trend across neurology devices.

3. Telemedicine infrastructure

COVID-19 did not create remote patient monitoring, but it accelerated adoption by years. Implantable remote monitoring devices now span cardiovascular, musculoskeletal, respiratory, gastrointestinal, and brain-monitoring applications. The ecosystem for connected devices finally has the bandwidth to scale.

Where the Growth Is Happening

In smart orthopedics, the knee segment leads. That makes sense. Total knee replacements are among the highest-volume orthopedic procedures globally, and outcomes depend heavily on implant positioning and patient compliance with rehab. Smart implants that track range of motion and loading in real time offer clear, measurable clinical value.

The spine and hip segments are also growing fast, fueled by demand for minimally invasive surgery and robotic-assisted implant placement. Asia-Pacific is the fastest-growing region, driven by expanding healthcare infrastructure and a rapidly aging population.

Beyond orthopedics, the picture is just as dynamic:

- Remote cardiac monitoring is surging, with the global cardiac monitoring market growing at a CAGR exceeding 10%.

- Neurology devices are incorporating AI, wearable sensors, and brain-computer interfaces into platforms that used to be purely surgical.

- Drug-device combinations are blurring the line between medtech and pharma, with wireless implants and smart drug delivery systems emerging as key frontiers.

The Hard Questions You Cannot Ignore

For all its promise, the connected implant wave brings real challenges. And the companies that dodge them will pay the price.

Cybersecurity tops the list. A connected implant is a networked device inside a human body. That is an extraordinary attack surface. The FDA has ramped up premarket cybersecurity requirements, and the EU’s Medical Device Regulation (MDR) now includes explicit provisions for software-driven devices. BCC Research identifies data privacy and cybersecurity as a key market restraint. Manufacturers that treat this as an afterthought will face regulatory delays and, worse, patient safety risks.

Reimbursement is uneven. Smart implants cost more to develop and manufacture. If payers do not recognize the downstream value (fewer revision surgeries, earlier interventions, reduced readmissions), the price premium becomes a barrier. This is especially true in emerging markets where economic constraints already limit device adoption.

Interoperability is the sleeper issue. As hospitals layer connected devices across departments, fragmented data standards and EHR integrations create friction. The companies that solve interoperability across the broader health IT stack, not just within their own product lines, will build a durable competitive moat.

What This Means for You

If you are a medtech leader, here is the bottom line: your company is no longer just a hardware manufacturer. You are now a software company, a data company, and a cybersecurity company.

The traditional playbook of iterative product improvement and GPO-driven distribution still matters. But it is no longer enough.

The winners in this next phase will invest in three areas at once:

- Sensor and data platforms that create clinical value beyond the implant itself

- Regulatory strategies that treat cybersecurity, data governance, and post-market surveillance as core competencies, not compliance checklists

- Ecosystem partnerships with health IT vendors, telehealth platforms, and payers that unlock outcome-based reimbursement models

Major players like Stryker, Zimmer Biomet, Johnson & Johnson, Medtronic, and Smith+Nephew are already making big bets here. Startups like Statera Medical, DirectSync Surgical, and Restor3D are challenging incumbents with sensor-first architectures and 3D-printed, patient-specific solutions.

The competitive landscape is shifting. Fast.

The Bottom Line

The connected implant is not a product category. It is a paradigm shift that touches every part of the medtech value chain, from R&D to post-market surveillance.

The market data is compelling: billions of dollars in growth, strong clinical tailwinds, and an aging global population that needs more devices, for longer, with better outcomes.

But the companies that win will not be the ones that simply bolt a sensor onto an existing product. They will be the ones that rethink the entire relationship between the device, the patient, and the healthcare system.

That is the real promise of the connected implant. And it is only getting started.

Want to explore what connected devices mean for your market segment? Get in touch and let’s discuss how these trends map to your portfolio and competitive landscape.